Taxation of Group Benefits

Federal Goods and Services Tax (GST)

- The Goods and Services Tax/Harmonized Sales Tax (GST/HST) is not charged on insured benefits.

- The tax is charged on the Administration Fee (only) under self-insured plans which do not contain any element of insurance.

- The federal government charges 7% GST on the administration charges for benefits.

Provincial Premium Tax (PPT)

- Insurance Tax, more commonly referred to as Premium Tax, is applicable to every insurance company in Canada.

- The tax is built into the premium, or charged on plan costs for self-insured plans.

- The rate varies by province and currently range between 2% and 4%.

- Ontario charges 2% Provincial Premium Tax on the cost of group life and health benefits.*

- Quebec charges 2.35% Provincial Premium Tax on the cost of group life and health benefits.*

- Nova Scotia and Newfoundland charge 4% Provincial Premium Tax on funded life and health benefits.

* Provincial Premium Tax (PPT) is also charged on the PPT if it forms part of the premium billed by an insurer.

Provincial Retail Tax (RST)

- Retail Sales Tax (RST), also referred to as Provincial Sales Tax (PST), is only applicable in Ontario and Quebec.

- The tax is charged on the premium, or plan costs, on all plans regardless of whether they are insured or self-insured.

- Ontario charges 8% Retail Sales Tax on group life and health benefits.*

- Quebec charges 9% Retail Sales Tax on group life and health benefits.

* Retail Sales Tax is also charged on the Provincial Premium Tax if it forms part of the premium billed by an insurer.

Provincial Income Tax

The employer portion of health and dental premiums is included in the tax base for Quebec.

The employer portion of health and dental premiums is included in the tax base for Quebec.

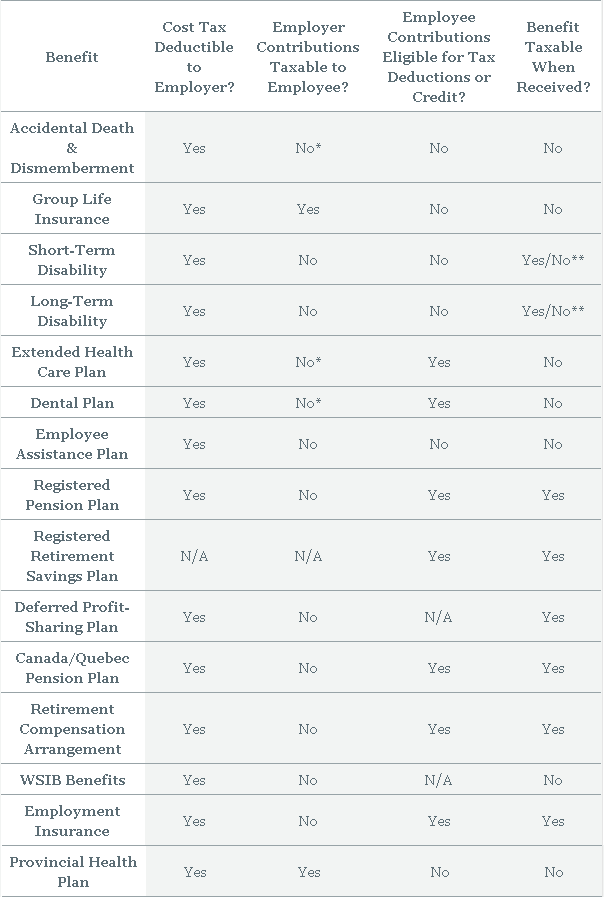

Income Tax Treatment of Employee Benefits

* Yes for Quebec

** Yes, if any part of the short-term or long-term

disability premium is paid by the employer. No, if the entire short-term or long-term disability premium is paid by the employee. Where the

costs of the short-term or long-term disability plan are shared between employer and employee, the employee is entitled to receive benefits

equal to his/her contributions on a non-taxable basis.